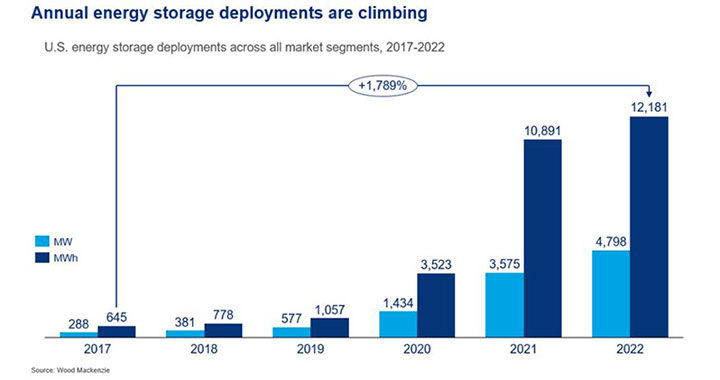

The US energy storage sector deployed 4.8GW in 2022, close to the combined amount installed in 2020 and 2021, despite a “slight dip” in install figures towards the end of last year.

The figure comes from the latest edition of the US Energy Storage Monitor, authored by market research firm Wood Mackenzie Power & Renewables (WoodMac) and published in partnership with the American Clean Power Association (ACP) trade group.

The report is quarterly, but the newest edition, for Q4 2022, rounds up some of the headline statistics and trends for last year.

In 2020 and 2021, 5GW of energy storage was deployed across all market segments, making 2022 the “best year yet,” according to ACP vice president of research and analytics John Hensley.

“Cumulative operating utility-scale storage capacity increased by 80%. While we saw a slight dip in installations toward the end of the year, the trend is clear: Energy storage is on a rapid growth curve and is already a key component of building a resilient grid that supports abundant clean energy,” Hensley said today.

In the fourth quarter of last year, 1,067MW was added across the different segments: grid-scale, residential and non-residential (representing commercial and industrial, and community-scale projects).

While that’s still more than has been seen in all but four of the most recent quarterly reports since Q4 2020, it was a 26% decrease from Q3 2022 and 514MW fewer than in Q4 2021, which was the biggest quarter recorded to date with 1,581MW.

A slowdown in the US grid-scale sector, which traditionally accounts for the bulk of deployments by far is the main reason for that dip. 848MW of grid-scale deployments were recorded over the three months between September and December, which compares unfavourably with Q3 2022’s 1,257MW of grid-scale and Q2’s 1,204MW.

Regular readers of this site will perhaps be unsurprised to note that WoodMac analysts ascribed this downturn to two primary factors: interconnection constraints and supply chain-related delays or difficulties in procuring equipment.

WoodMac said more than 3GW of projects due to come online in Q4 2022 had been either delayed or cancelled. Added to projects already known to be delayed or cancelled prior to that, it accounts for 7GW in total, which the firm said is most likely due to developers being unable to procure equipment in the timeframe required by their contracts or business case, or due to increased costs.

The analysis firm noted that grid-scale battery energy storage system (BESS) costs went up year-on-year, from US$1,636/kW in Q4 2021 to US$1,933/kW in Q4 2022, an increase of 18%.

Nonetheless, the pipeline of grid-scale projects has grown significantly, by 53% from 302GW of combined announced projects and projects in interconnection queues in the final quarter of 2021, to 463GW in the final quarter of 2022.

The numbers of projects waiting interconnection far outweighed announced projects in both cases. That being said, the volume of queuing projects seeking connections between 2023 and 2028 declined by about 10% from the previous quarter. Independent system operators (ISOs) that operate wholesale markets as well as grids have begun filtering out applications that don’t meet required standards, while some developers have withdrawn applications after a rush to secure queue positions subsided.

In megawatt-hour terms, that 1067MW of Q4 deployments meant 3,030MWh of new energy storage capacity, with 2,506MWh of that at grid-scale.